Employer Reporting of Health Coverage – Code Sections 6055 & 6056

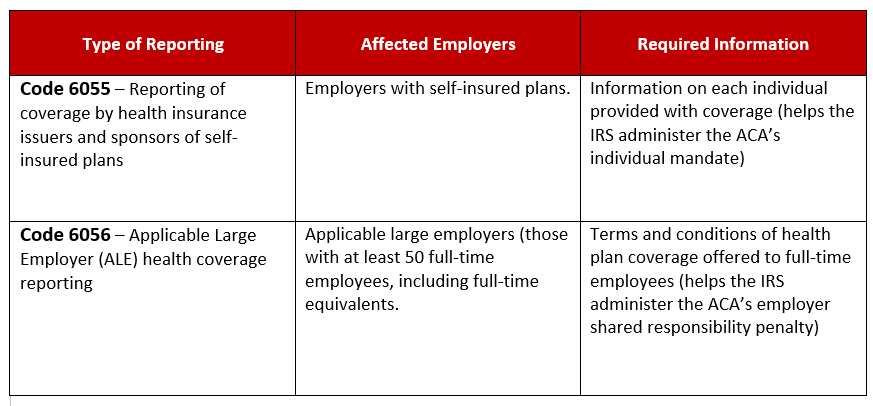

The Affordable Care Act created new reporting requirements under Internal Revenue Code Sections 6055 & 6056. Under new reporting rules, certain employers must provide information to the IRS about the health plan coverage they offer (or do not offer) to their employees. The additional reporting is intended to promote transparency with respect to health plan coverage and costs. It will also provide the government with information to administer other ACA mandates, such as the large employer shared responsibility (pay or play) and the individual mandate.

- Form 1094-B and Form 1095-B will be used by entities reporting under Section 6055, including sponsors of self-insured group health plans that are not reporting as ALEs

- Form 1094-C and Form 1095-C will be used by ALEs that are reporting under Section 6056, and for combined reporting by ALEs that sponsor self-insured plans required to report under both Sections 6055 and 6056.

LaPorte is proud to offer guidance on these new reporting guidelines. Our client partners receive personal assistance and tools specific to efficiently satisfy this difficult compliance requirement.